© Copyright 2026, Monarch Wealth Strategies. All Rights Reserved.

Key Tax Changes to Be Aware of in 2026

Monarch Wealth Strategies | December 1, 2025

With provisions in the One Big Beautiful Bill Act (OBBBA) and new inflation-adjusted amounts announced by the IRS, taxpayers can expect various tax changes in 2026. Being aware of these shifts can help you develop more effective tax management strategies for income timing, charitable donations, retirement contributions, and deductions. Here are the key changes you can discuss with your CPA and wealth advisor as you head into the new year.

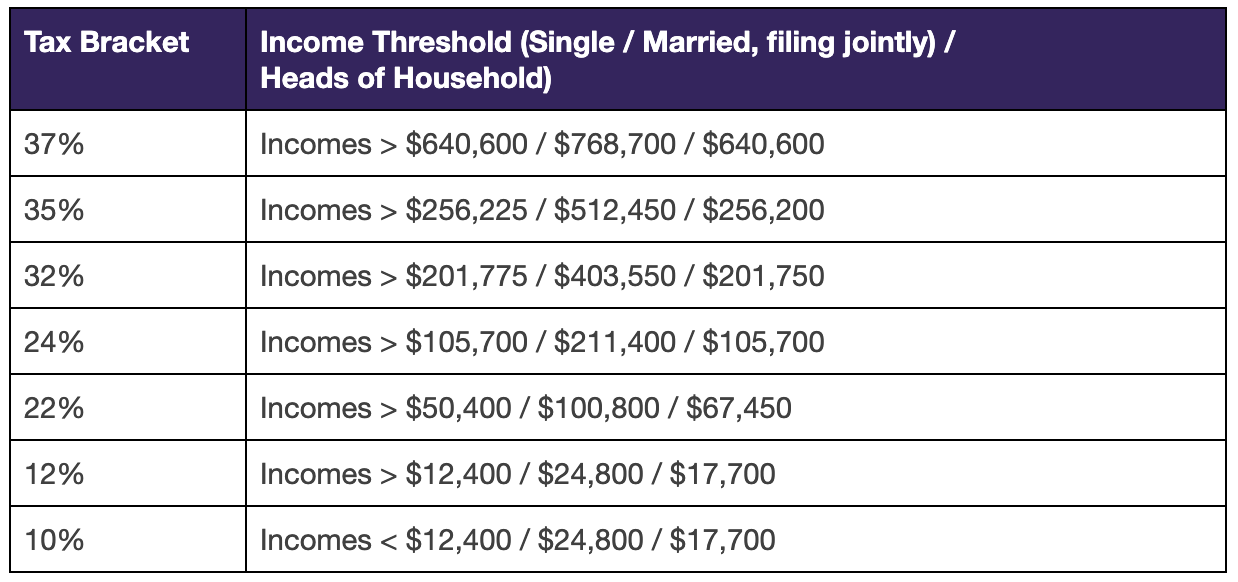

New Tax Brackets

The IRS recently announced inflation-adjusted tax bracket thresholds for 2026, giving taxpayers additional earning flexibility before moving into a higher bracket.

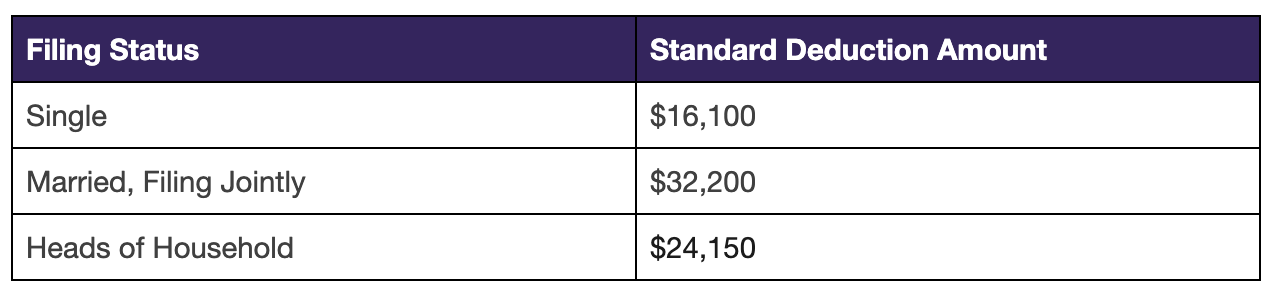

New Standard Deductions

As part of the OBBBA, the new standard deduction in 2026 will increase.

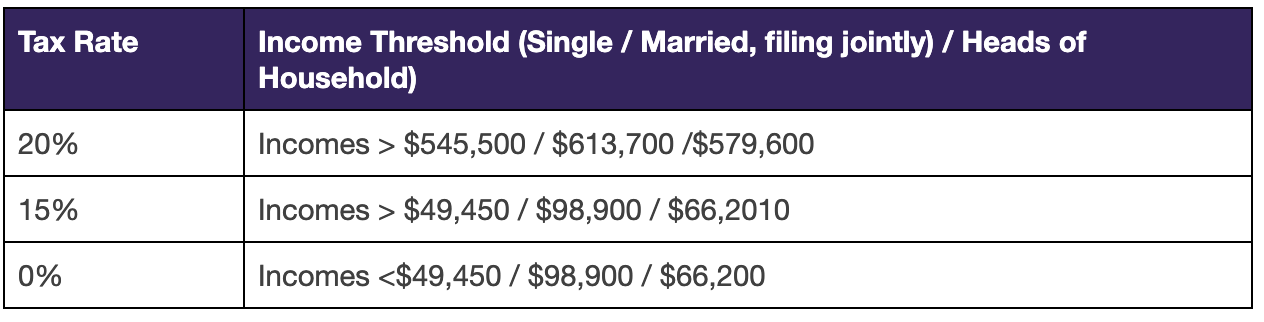

New Capital Tax Rates

Effective in 2026, the following new rates will apply to long-term capital gains.

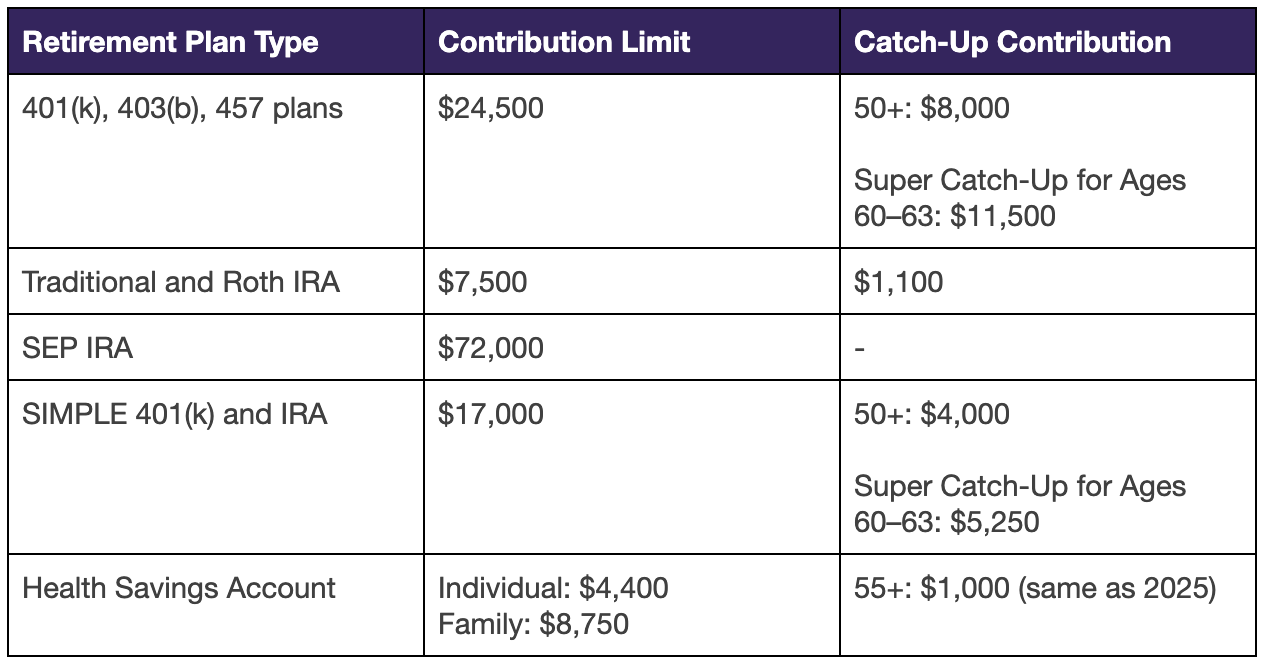

New Retirement Plan Contribution Limits

Contribution limits on retirement plans are also increasing to address inflation.

Qualified Business Income Deduction

The 20% deduction for certain pass-through business income is now permanent, with additional changes, including:

- Wage/property limits and specified service trade or business (SSTB) exclusions are increasing:

- Single filers: $75,000 income threshold

- Married couples: $150,000 income threshold

- There is a new guaranteed minimum qualified business income (QBI) deduction of $400 for business owners who generate at least $1,000 of QBI from an active trade or business, as long as they materially participate.

New Charitable Deduction

In 2026, there will be tax changes for charitable giving, which may require evaluating whether itemizing or non-itemizing deductions make financial sense for you:

- If You’re Non-Itemizing: New deduction of $1,000 for singles and $2,000 for joint filers.

- If You’re Itemizing: A new deduction floor will require donations to be above 0.5% of adjusted gross income.

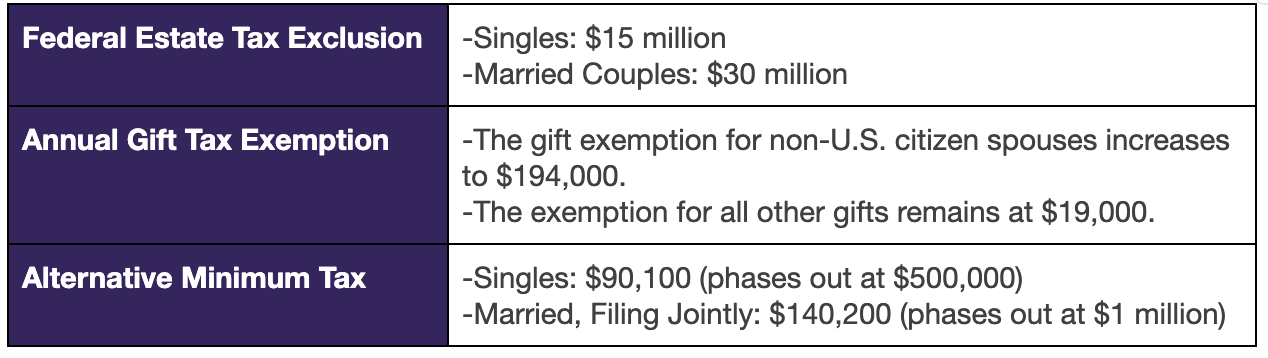

Increased Tax Exemptions

Exclusions for the federal alternative minimum tax, estate tax, and certain gifts will increase in 2026, which might be meaningful for high-income earners and business owners, including:

Temporary Tax Provisions

There are also time-bound tax provisions introduced in the OBBBA that began in 2025 and will expire in the coming years you should be aware of, should you reach the qualifying age or your financial situation changes, including:

- State and Local Tax (SALT) Deduction Increase (through 2029): The SALT deduction cap has temporarily increased to $40,000 (up from $10,000).

- New Senior Tax Deduction (through 2028): Available to those 65 and older, eligible taxpayers can take an additional $6,000 or $12,000 for joint filers, with phase-outs beginning at $75,000 for singles and $150,000 for married, joint filers.

- Tax Deduction on Tips (through 2028): The deduction is $25,000, phasing out at $150,000 for singles and $300,000 for joint filers.

- Tax Deduction on Overtime Pay (through 2028): The deduction is $12,500 for singles or $25,000 for joint filers, phasing out at $150,000 or $300,000, respectively.

Navigating the Evolving Tax Landscape with Monarch Wealth Strategies

As the tax environment changes, it’s essential to review your strategy to identify opportunities and considerations, such as:

- How to prevent exceeding income thresholds through income timing, charitable donations, and retirement plan contributions.

- If itemizing or non-itemizing deductions is more optimal for you.

- If the new senior tax changes will affect your required minimum distributions or the timing of a Roth conversion.

While we do not offer tax advice, we are happy to collaborate with you and your tax professional to develop a comprehensive plan that integrates and optimizes all aspects of your financial life. Please contact us if you have questions about your situation, the forthcoming changes, or how to connect with a trusted CPA.

For more information about the changes, view our recent blog post about navigating the OBBBA.